Workflow Is Power: Have Banks Lost The Moment of Decision in B2B Payments?

In theory, banks should own B2B payments.

They already serve the customers. They manage the accounts. They control the rails. No player is better positioned—on paper.

But in practice, it’s platforms like Melio, Airbase, and Ramp that are winning the workflows, capturing the margin, and setting the pace.

They’re not doing this because they have superior balance sheets or better regulatory standing.

They’re doing it because they sit closer to intent.

Imagine two people:

- Person A owns the train tracks.

- Person B owns the train station where tickets get bought.

Who controls the journey? The one who owns the moment of decision.

In B2B payments:

- The bank owns the wires, the vaults, the rails.

- The platform owns the click that says: “Pay this supplier now.”

Control shifts not through ownership of infrastructure—but through ownership of workflow initiation.

They’ve figured out something most banks haven’t:

In B2B, the firm that owns the trigger—the moment a payment is initiated—owns the value chain.

That’s where the real leakage is happening.

The gap between what banks offer and what businesses need is growing wider. This is especially evident in the middle market across logistics, trade, and vertical SaaS.

And for financial leaders in those emerging mid-markets, it’s to redefine how institutional trust is distributed across the ecosystem.

Banks have a massive advantage in B2B payments; it's theirs to lose if they remain complacent.

The Endpoint Problem

Banks are increasingly investing in workflow integration, APIs, and partnerships with SaaS providers to embed financial services where business decisions are made. However, many banks have historically focused (and continue to focus) on endpoints, like accounts and transaction types.

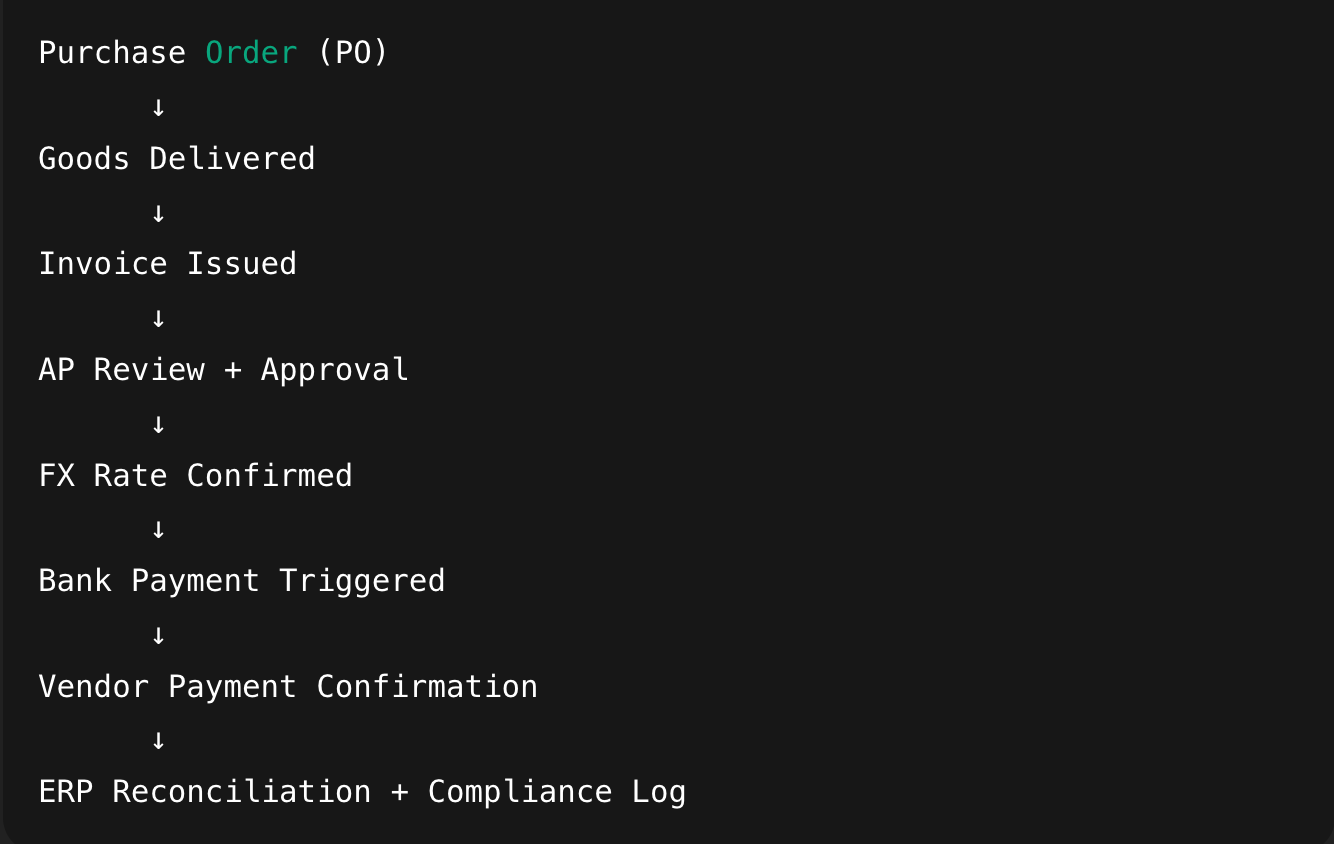

But B2B firms don’t operate in endpoints. They operate in flows: from PO to invoice, from FX approval to payout confirmation, and from compliance check to partner dashboard. These aren’t abstract events; they’re daily operational rhythms.

The moment those rhythms are broken, trust erodes.

A delayed wire to a supplier in Nairobi.

A missing approval on an invoice in Durban.

A treasury team unsure whether a USD payout was routed correctly before quarter close.

None of these things are failures of funds movement. They’re failures of system design.

Banks control the rails, but they don’t control the logic that surrounds them.

The logic now lives upstream—in ERPs, vertical SaaS platforms, procurement tools, and embedded dashboards.

These are the systems where business users live.

These are the tools that structure the emotional flow of a transaction: is it fast, clear, trustworthy—or anxiety-inducing?

What Friday Feels Like

To understand what’s broken, start at 4:45pm on a Friday.

A controller is rushing to release payments. They’re toggling between a spreadsheet, a cumbersome ERP, an internal Slack thread, and a browser tab with the bank’s treasury portal.

There’s a WhatsApp message from a vendor in Lusaka asking about a late invoice.

There’s an unresolved FX quote from earlier in the day.

They approve what they can and leave the rest for Monday.

This is what B2B finance teams live through weekly.

Each additional click increases the anxiety:

- “Did I send the right amount?”

- “Will it clear in time?”

- “Will this come back to bite me?”

This is the emotional tax of bad payment infrastructure.

And most platforms ignore it.

It’s not that business users can’t handle complexity. They handle it every day. But they resent systems that make them feel unsafe while doing it.

Some banks think their systems are robust when in reality, they’re fragile. Not because the rails don’t work—but because the user has no idea what’s happening between the click and the confirmation.

Misaligned Success Metrics

Many banks still measure progress in terms of product penetration: number of clients using ACH, wire volumes, FX contracts signed.

But their clients—especially in the middle market—measure success in entirely different ways:

- Did the vendor get paid without chasing us?

- Was the CFO able to sign off with confidence?

- Did we avoid another 11pm reconciliation scramble?

- Are we out of the red on currency exposure?

This misalignment creates enormous white space.

When you reward internal teams for selling more products, you create friction for the customer. Teams don’t optimize for coherence. They optimize for quota.

Reframe success not around what the bank delivers, but around how seamlessly it integrates with the work customers already do.

Create interventions that reduce noise.

Treat simplicity not as a UI issue but as a core financial deliverable.

Infrastructure Without Empathy Doesn’t Scale

Many banks believe modernization is blocked by legacy cores. And in some ways, they’re right.

But infrastructure is only half the story.

The deeper issue is proximity to emotion.

Consider this:

A $5M bank API investment might increase throughput. But if the business user still has to manually confirm FX rates by email and chase approvals in Slack, the experience still feels broken.

The real leverage lies in layering empathy into the infrastructure:

- Offer a routing engine that can dynamically shift between local rails, SWIFT, and stablecoins—based on corridor friction.

- Design a message layer that sends payout confirmations into WhatsApp or Slack—because that’s where users actually check.

- Build a feedback loop between buyers and vendors on each transaction—to surface dispute risks before they hit support.

None of this requires a new core.

It requires a new perspective.

One that sees payment infrastructure not just as plumbing, but as a behavioral trust system.

The Firms That Win Own the First Click

This is the pattern that fintechs understood early:

Whoever owns the first click—the one that initiates a payment, approves a payout, sends a vendor invite—owns the experience.

And increasingly, that click isn’t happening in bank portals.

It’s happening in vertical platforms. Procurement tools.

Embedded modules inside the tools customers already use.

That’s why firms like Ramp and Airbase don’t fight for the last mile. They fight for the first touch.

They shape how the transaction feels. They reduce friction before it even shows up. And they make the user feel competent, not confused.

If banks want to reclaim this ground, they need to stop thinking in endpoints and start building interfaces of trust.

Tools that live where decisions get made.

Systems that collapse the gap between financial logic and emotional confidence.

Design for Relief, Not Just Compliance

A few years ago, a CFO at a freight platform we advised did not trust their systems.

The team wasn’t afraid of the technology. They were afraid of making a mistake inside the technology.

So we restructured their flow—not by swapping software, but by mapping emotional tension points across the process.

We made payout statuses visible inside the tools they were already using. We sent real-time FX locks to Slack. We moved vendor onboarding out of PDFs and into embedded, trackable flows.

The impact:

📉 Ticket volume dropped 62%.

💸 DSO improved by 11 days.

📉 Vendor churn in low-trust corridors dropped by double digits.

Get Closer to the Work

The banks that will win the next decade of B2B aren’t necessarily the ones with the most products or largest balance sheets.

They’re the ones who get closer to where the work actually happens.

That means embedding into flows—not waiting at the end of them.

It means designing for trust—not just compliance.

It means treating UX not as a frontend skin—but as a core liquidity enabler.

Final Thought

Banks haven’t lost relevance as they remain large players in global commerce.

They’ve lost workflow proximity.

And unless that changes, B2B clients will continue to shift their trust to platforms that sit closer to the action—even if those platforms move the money through bank rails behind the scenes.

The opportunity is to re-enter the workflow. Not with dashboards or PDFs—but with systems that reduce tension, restore confidence, and reclaim the emotional territory that banks once owned by default.